By Brian Bloxom, ChFEBCSM

For many investors, it may seem tempting to try to “time the market” and buy low and sell high. This, after all, is the golden rule of investing. But what do financial advisors who specialize in comprehensive planning recommend?

While it can be tempting to try your hand at timing the market, the truth is it doesn’t actually work. Here are 3 reasons why and what you should do instead.

Market Timing Is Consistently Inconsistent

Timing the market usually involves attempting to “buy low and sell high” by analyzing current market trends for inefficiencies or volatility indicators. This strategy may work sometimes, but it is far from perfect. Not only do you have to guess when to buy in, but you then have to guess when to sell. That means for every gain, you have to be right twice to make timing the market worth it. Unfortunately, market bottoms can only be truly spotted in hindsight, and timing the market is often closer to playing the lottery than it is to an educated guess.

Timing the Market Is Expensive

Timing the market can also be expensive. Depending on your account type, asset class, and where you are executing your trades, you will likely be charged for every purchase and sale you make, and that’s on top of any taxes owed on gains. The more frequently you trade, the higher your transaction costs will be.

If you held the assets for less than a year, your gain will be taxed as ordinary income at your marginal tax rate, which can be as high as 37% for high-income earners. Long-term gains are taxed at a preferential rate. Regardless of your tax rate, your market timing must still be right more often than not just to cover the cost of your guess.

You Will Miss Out on Compound Growth & Market Rebounds

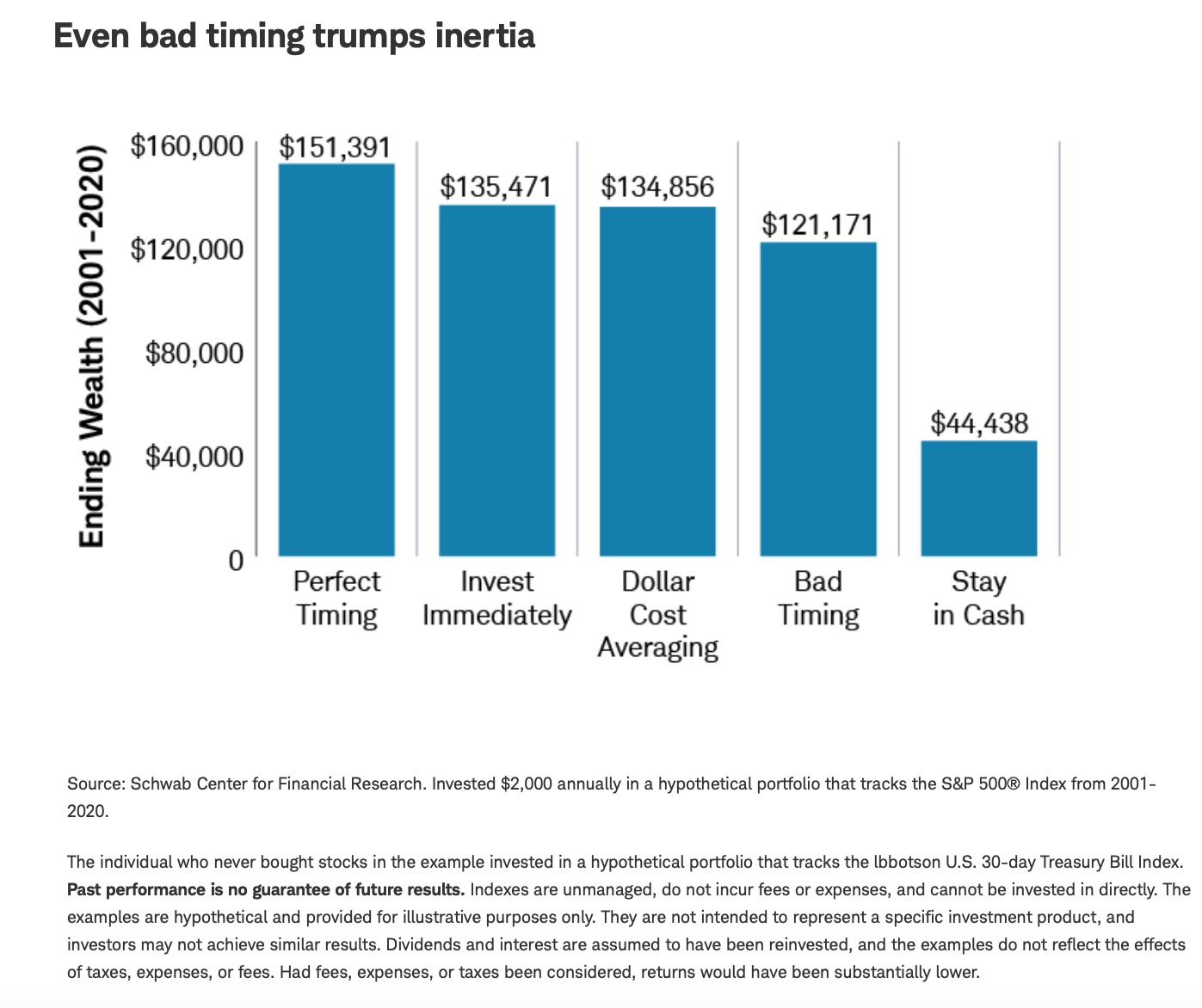

A recent study by Schwab Center for Financial Research found that bad market timing is worse than investing immediately, regardless of the market conditions at the time of investing. This indicates that even in market downturns, or just before a downturn, investors who invest immediately and remain invested will be better off than those who stay on the sidelines or attempt to time the market.

Take a look at Schwab’s graph below, which shows just how much more a fully invested portfolio earns over the course of 19 years. It would earn approximately $14,000 more in growth than a portfolio with bad market timing, and $91,000 more than a portfolio that stays in cash. The only investor who performs better is the one with perfect timing—but since we already know that perfect timing is impossible, investing immediately is the next best strategy.

What’s more, over time that extra $14,000 or $91,000 will have the opportunity to grow even more thanks to compounded interest. Even if the market fluctuates in the short term, the odds are high that a solid investment strategy will grow over time.

Another graph by Hartford Funds and Morningstar shows what happens if you miss the best days in the market, which often closely follow a major downturn and can be just as difficult to predict. An investor who missed the 10 best days in the market between 1992 and 2021 would have earned 54% less than someone who was fully invested during the same time period.

Someone who missed the 30 best market days would have earned a whopping $172,000 (83%) less than their fully invested counterpart. The research is based on a $10,000 initial investment, but these numbers would be much more dramatic if you were dealing with a $100,000 or even a $1,000,000 portfolio.

The time value of money tells us that a dollar today is worth more than a dollar tomorrow, and this is certainly the case when it comes to investing. The longer you are invested, the more likely you are to ride out the day-to-day market fluctuations and experience growth instead.

Are You Missing Out on Opportunities for Growth?

Don’t cheat yourself out of opportunities for growth by trying to time the market. Instead, focus on a long-term strategy based on your goals. At Sentinel Wealth Partners, we have a passion to serve you and see you retire comfortably, so we get to know you before recommending and managing your investments. When making decisions, we take into account your short-term and long-term goals, your resources, and your current situation. Reach out to us today by calling our office at 703-832-0164, sending an email to [email protected], or using our online calendar.

About Brian

Brian Bloxom is an Independent Financial Advisor, Chartered Federal Employee Benefits ConsultantSM (ChFEBCSM) and Chartered Retirement Planning Counselor℠, CRPC® professional with 25 years of experience in financial advising. He founded Sentinel Wealth Partners to serve retirees, individuals approaching retirement, and individuals managing complex retirement plans such as company plans or federal benefits plans. His expertise and dedication to helping his clients achieve their goals make him a trusted resource that will help you feel confident in your customized retirement plan. Brian’s mission is to be available to his clients—all the time. He’s here to solve your problems, relieve your anxiety, and give you optimism for retirement. Because ultimately, your retirement should be about well-deserved enjoyment, and not about stress or anxiety. When he’s not working, you can find Brian spending time with his wife, Jessica, and their two sons, Spencer and Preston. He enjoys coaching soccer, serving in his community, golfing, and relaxing at his vacation home at Lake Anna, VA. To learn more about Brian, connect with him on LinkedIn.